MBS Road Signs 12-15-2025

MBS Road Signs 12-15-2025

Week of December 8, 2025 in Review

The Fed announced its third rate cut of the year, while more labor data pointed to underlying softness in the job market. Here’s a look at the key highlights.

Fed Delivers Third Rate Cut as Policymakers Split

Job Openings Tick Higher, Yet Underlying Weakness Persists

Claims Data Skewed by Holidays and Benefit Expirations

What to Look for This Week

Technical Picture

Fed Delivers Third Rate Cut as Policymakers Split

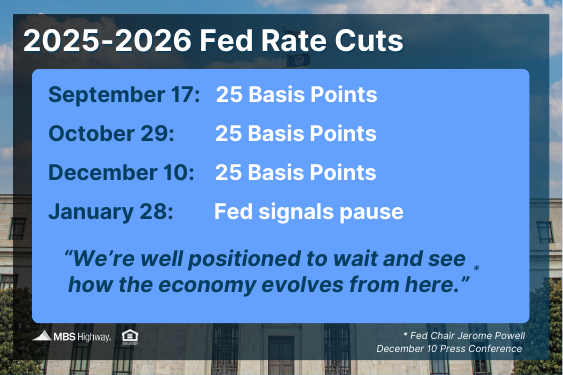

The Federal Reserve cut the benchmark Federal Funds Rate by 25 basis points to a target range of 3.50% to 3.75%, its third reduction this year. The Fed Funds Rate – what banks charge each other for overnight loans – doesn’t directly set mortgage rates but does influence borrowing costs across the economy.

The move wasn’t unanimous. Governor Stephen Miran pushed for a bigger 50-bp cut, while Kansas City’s Jeffrey Schmid and Chicago’s Austan Goolsbee wanted to hold rates steady – highlighting the Fed’s challenge of managing elevated inflation alongside a softening job market.

What’s the bottom line? Chair Jerome Powell stressed that there’s “no risk-free path,” signaling that policymakers may need stronger evidence before approving further cuts as they balance labor-market risks against inflation pressures.

Fresh projections underscore the internal debate: six of nineteen officials supported holding rates steady at this meeting, likely reflecting hesitation among both voting and nonvoting members. For next year, the median forecast points to at least one additional 25-basis-point cut, but the outlook may shift as a new cohort of voting members rotates in.

Job Openings Tick Higher, Yet Underlying Weakness Persists

Delayed data for September and October showed job openings coming in stronger than expected – rising from 7.23 million in August to 7.66 million in September and 7.67 million in October. However, the headline figure may be inflated, as many remote positions are posted across multiple states.

What’s the bottom line? Despite the recent uptick, job openings remain well below the 2022 peak of more than 12 million, and the underlying metrics point to continued cooling. The hiring rate (3.2%) is tied for its lowest level since 2011 outside the pandemic.

Layoffs have risen to their highest since January 2023, and the quit rate (1.8%) is at its lowest since 2014 (again excluding the pandemic), signaling weaker demand for workers and less confidence among employees to switch jobs.

Another sign of the slowdown: the ratio of job openings to unemployed workers has fallen from over 2:1 in 2022 to roughly 1:1 today.

Claims Data Skewed by Holidays and Benefit Expirations

Initial jobless claims rose by 44,000 to 236,000, the highest level since September, following an unusually low reading during Thanksgiving week. Continuing claims, which lag initial claims by one week, fell sharply by 99,000 to 1.84 million.

What’s the bottom line? The large drop in continuing claims was likely driven by holiday-related distortions and expiring benefits. The reference week for continuing claims included Thanksgiving, when holiday travel can suppress filings. In addition, most states provide up to 26 weeks of benefits; looking back that far, a spike in initial claims last May and early June means many recipients may now be reaching the end of eligibility.

Together, data quirks and benefit expirations likely explain the sharp decline.

What to Look for This Week

Housing data kicks off and ends the week, with NAHB home builder confidence on Monday and November’s Existing Home Sales on Friday. We’ll also get several government reports delayed by the shutdown, including the Jobs Report and Retail Sales on Tuesday, followed by the Consumer Price Index on Thursday.

Technical Picture

Mortgage Bonds ended last week below support at both the 25 and 50-day moving averages. The 10-year Treasury yield tested resistance at 4.20%, which continues to hold, and finished the week trading between that ceiling and support at its 100-day moving average. With inflation and jobs data finally set for release after the shutdown, markets could see impactful movement ahead.